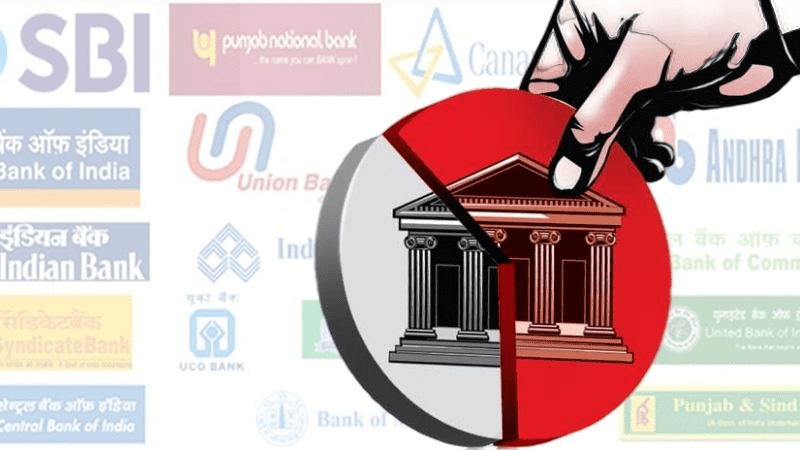

About the Laxmi Vilas Bank - DBS Bank India merger

It was a cold, not so eventful evening of November 17 when I received a news alert on my phone. The alert read ‘Breaking News: RBI puts Lakshmi Vilas Bank under a moratorium for 30 days, restricts withdrawals to Rs 25,000 ‘. It was later announced that it will be merged with DBS Bank India, the Indian wing of the Singaporean banking giant, DBS Bank.

Now, after almost a month, Lakshmi Vilas Bank (LVB) has been merged with DBS Bank India. Given the continued decline of the bank’s financial standing and the absence of a concrete revival plan, RBI had to step in and take matters in its own hands, and opt for the merger.

India’s apex bank said, “The financial position of The Lakshmi Vilas Bank Ltd has undergone a steady decline with the bank incurring continuous losses over the last three years, eroding its net-worth. In absence of any viable strategic plan, declining advances and mounting non-performing assets (NPAs), the losses are expected to continue. The bank has not been able to raise adequate capital to address issues around its negative net-worth and continuing losses. Further, the bank is also experiencing continuous withdrawal of deposits and low levels of liquidity.” The RBI also stated that LVB experienced serious governance issues and practices in recent years which led to a deterioration in its performance. The bank was placed under the Prompt Corrective Action (PCA) framework in September 2019 considering the breach of PCA thresholds as on March 31, 2019.

Keeping in mind the situation of the depositors of LVB and their future, RBI further said, that it assures the depositors of the bank that their interest will be fully protected and there is no need to panic. “In terms of the provisions of the Banking Regulation Act, the Reserve Bank has drawn up a scheme for the bank’s amalgamation with another banking company. With the approval of the Central Government, the Reserve Bank will endeavour to put the Scheme in place well before the expiry of the moratorium and thereby ensure that the depositors are not put to undue hardship or inconvenience for a period of time longer than what is absolutely necessary,” it said.

Keeping in mind the situation of the depositors of LVB and their future, RBI further said, that it assures the depositors of the bank that their interest will be fully protected and there is no need to panic. “In terms of the provisions of the Banking Regulation Act, the Reserve Bank has drawn up a scheme for the bank’s amalgamation with another banking company. With the approval of the Central Government, the Reserve Bank will endeavour to put the Scheme in place well before the expiry of the moratorium and thereby ensure that the depositors are not put to undue hardship or inconvenience for a period of time longer than what is absolutely necessary,” it said.

Merger Complete: The Road Ahead

On November 30, DBS Bank announced the completion of the merger. “Lakshmi Vilas Bank (LVB) is now amalgamated with DBS Bank India Limited (DBIL), the wholly-owned subsidiary of DBS Group Holdings Ltd. The moratorium imposed on LVB was lifted from 27 November 2020 and banking services were restored immediately with all branches, digital channels and ATMs functioning as usual,” said the Singaporean banking giant. It also said that DBS Group will additionally inject Rs 2,500 crore (SGD 463 million) into DBIL to support the amalgamation and for future growth, and it will be fully funded from DBS Group’s existing resources. This successfully closed the chapter of erstwhile LVB and saved its depositors from going under.

NPAs, Bad Loans and Write-Offs: What are they?

These are a few terms which are found in any report that deal with banks and other financial institutions undergoing crises. Every time a bank is in news, for good or bad reasons, ample focus is given on NPAs, their existing bad loans and how big were the write-offs in the recent past.

If you look carefully at a balance sheet of a bank, you will see two columns: assets and liabilities. Speaking strictly in terms of macroeconomics, an asset is something of value that is owned and can be used to produce something, while liabilities are things that are owed to outsiders.

Bank loans fall under the category of assets as they fetch interest, while the deposits which the public lodge in the bank are liabilities, as banks shell out interest on them. There are many other instruments which fall under the columns of assets and liabilities, but we won’t be going deep in detail about them.

When a bank loan is defaulted by the borrower or interest payments are delayed for a prolonged period - fetching less or no interest to the bank, then that loan is tagged as Non-Performing Asset (NPA). A loan is said to be in default when the lender considers the loan agreement to be broken and the borrower is unable to meet his obligations. This usually happens when the borrower files for bankruptcy.

NPAs play a crucial role in determining the financial health of a bank. If the concentration of NPAs is too high, then it plays a negative role in the balance sheet of the bank and might attract the wrath of the regulators, in addition to putting the lender in much more financial jeopardy.

A bad loan on the other hand is a loan which is not being repaid as per original terms and conditions between the borrower and lender, and which might never get repaid. In business terms, it is the portion of a loan or portfolio of loans which is considered to be uncollectable. One of the most common causes of bad loans is when the borrower declares bankruptcy.

A write-off is a technical term which is deployed when the lenders run out of ways to collect the loans that were given out. Even though it does not signify the complete cancellation of recovery, it means that all ways of extracting the money have been exhausted. Write-offs also play a crucial role in determining the well-being of a bank or financial institution.

The Indian Story: How bad are the loans, and how many have been written off?

The Indian banking sector has been hit by multiple cases of NPAs and bad loans running into huge numbers, and many such have been written off as well. They put intense pressure on the balance sheets of the bank, and often have negative consequences. One of the most high profile cases of a bank being shaken to the core by bad loans was that of diamantaire Nirav Modi, who defrauded the Punjab National Bank of close to Rs 14,000 crore.

Pune based RTI activist Vivek Velankar’s recent findings on the NPAs of 12 Public Sector Banks (PSB) came as a big blow to the Indian banking sector and it exposed the intricacies that lied underneath the books and sheets. His findings were published by Money Life. Following is an excerpt which explains the entire NPA and write-off story:

"Over the past eight years, 12 nationalised banks have written off a massive of Rs. 6.32 lakh crores of bad loans. Of these, as much as Rs. 2 .78 lakh crore of the loans written off were to big defaulters with borrowings of Rs. 100 crore and above. While the government had aggressively claimed that loans written off are aggressively pursued and recovered, the recovery by these 12 banks from defaulters is just 7% or only Rs. 19,207 crore."

The Indian banking sector has gone through a tumultuous journey over the past year. From PMC Bank almost going under, to Yes Bank being saved by SBI in the last minute. All the stories have a few common plotlines and villains: unchecked and malpractice-ridden lending, taking more risks than what is feasible, and the lack of a watchdog and regulation. The lending policies and principles need to be checked, the downside of risk has to be properly evaluated and all the operations of banks need to be under proper and unbiased scrutiny of a regulator. These are a few of the ways to make sure the assets perform well, loans turn from bad to good, and the only thing that is written off a balance sheet is a typo.

- Akashdeep Baruah

baruah.akashd@gmail.com

(The author is an independent journalist who writes about pop culture, digital media, economy, and other related subjects. He has previously worked with organizations like Reuters and Times Now. Author's portfolio: www.muckrack.com/bforbaruah )

Tags: rbi laxmi vilas bank dbs bank loans write offs akashdeep baruah economy banking sector economics Load More Tags

Add Comment